Affordable Housing Sector: Implications of Large LIHTC roll-offs

As we progress through the year, the affordable housing market faces a critical juncture, with thousands of units across the nation approaching the end of their Low-Income Housing Tax Credit (LIHTC) and Section 8 contracts. The decisions made by property owners this year will have long-lasting effects on the landscape of affordable housing.

1. Understanding the Magnitude of Expiring Contracts

To grasp the gravity of the situation, it’s crucial to examine the data. Across various states, a significant number of affordable housing units are set to lose their government-subsidized status. This could lead to a substantial shift in the availability of affordable housing, particularly in high-demand markets.

Chart 1: Number of Affordable Units with Expiring LIHTC and Section 8 Contracts by State

- California: With 15,279 units expiring this year, California is at the forefront of this issue. A substantial portion of these units will expire in the final quarter, underscoring the urgency for action.

- New York: Close behind, New York sees 12,013 units expiring, with a notable spike in Q4. The state’s already tight housing market could be further strained if these units transition to market rate.

- Ohio: Ohio faces 11,734 units expiring this year, with significant numbers in Q1 and Q4. The decisions made in Ohio will have a lasting impact on the state’s affordable housing landscape.

- Texas: In Texas, 7,458 units are at risk, particularly in Q4. The state’s growing population and rising rents could encourage many owners to opt for market-rate conversions.

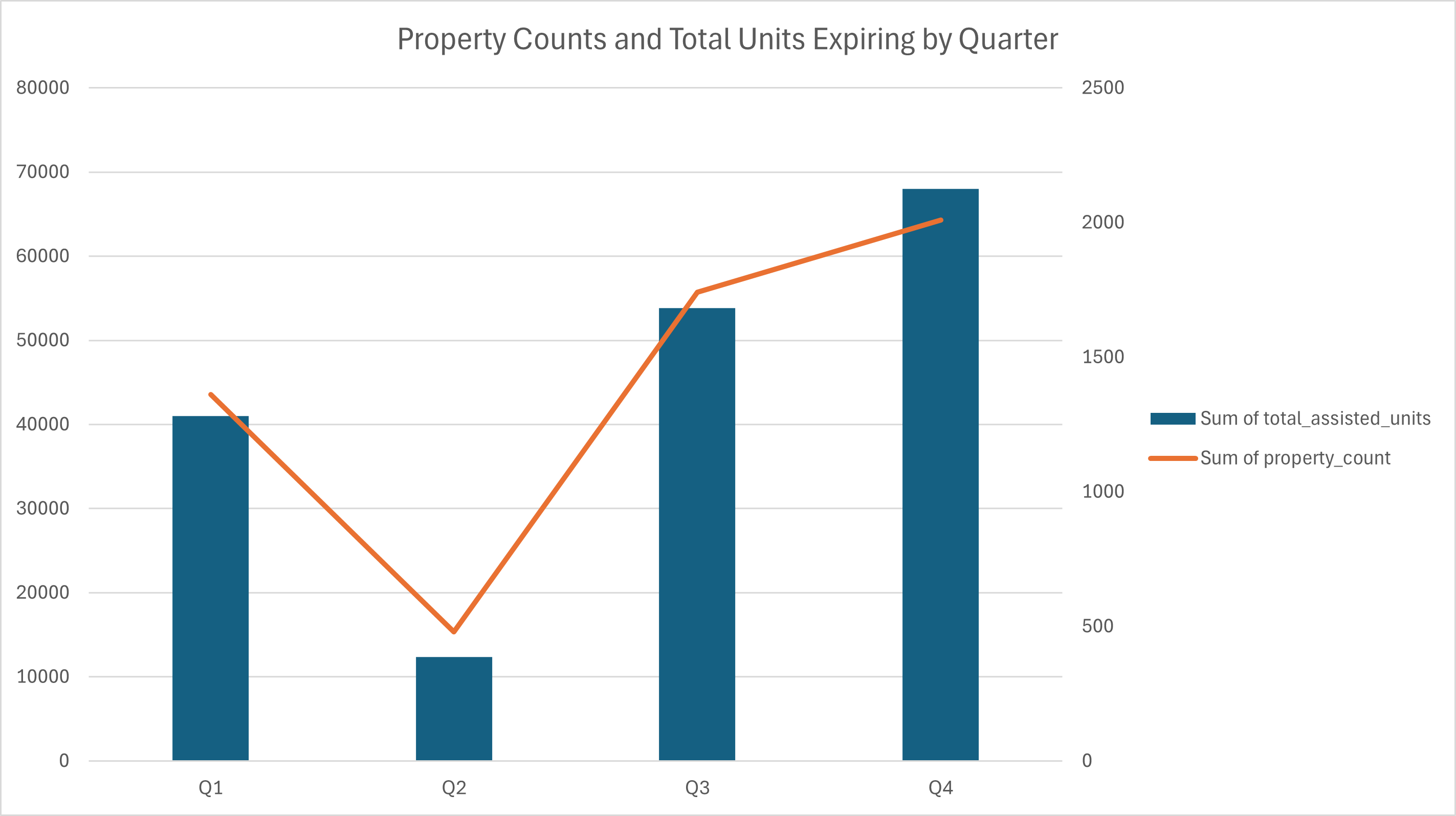

2. The Critical Q4 Crunch

The data reveals a significant trend: a large proportion of contracts are set to expire in the fourth quarter. This end-of-year concentration presents a potential crisis, as many property owners will be making decisions simultaneously.

Chart 2: Quarterly Distribution of Expiring Units

This Q4 peak suggests a possible sudden reduction in affordable housing supply if owners choose to convert their properties to market rate. Policymakers and housing advocates are likely prepared to address this potential surge in conversions.

3. Possible Outcomes: Renewal or Market Conversion?

With thousands of units on the line, property owners face a critical decision: renew their contracts with the government or convert their units to market-rate housing. The choice will depend on various factors, including local market conditions, the attractiveness of government subsidies, and the financial health of the properties.

- Renewal of Contracts: Many owners may opt to renew their contracts, especially in markets where affordable housing demand is high, and government incentives remain strong. This would maintain the current stock of affordable housing, albeit often at higher costs due to the need for property improvements or adjustments to contract terms.

- Conversion to Market-Rate: In markets with strong rental demand, some owners may decide to convert their properties to market-rate units. This trend is particularly concerning in states like New York and California, where housing affordability is already a pressing issue. The loss of these units would exacerbate existing shortages, leading to increased competition for the remaining affordable units and potentially driving up rents.

4. Regional Spotlight: States Most at Risk

While the impact of these expiring contracts will be felt nationwide, certain states are at greater risk due to the sheer volume of expiring units and the local housing market dynamics.

- California: With a significant portion of its affordable housing stock at risk, California could see a major reduction in affordable units, particularly in urban centers where market demand is high.

- New York/New Jersey: New York area faces a similar challenge, with a large number of units expiring in Q4. The state’s tight rental market and high property values could drive many owners to convert their units, further straining the availability of affordable housing.

- Texas and Ohio: Both states have large numbers of expiring units and rapidly growing populations. The decisions made here will have long-lasting implications for housing affordability in these states.

5. The Path Forward:

- Enhanced Incentives for Renewal: Governments at all levels may continue to provide additional incentives for property owners to renew their contracts. This might include increased subsidies, tax breaks, or grants for property improvements.

- Development of New Affordable Housing: To offset the potential loss of existing units, there likely maybe a concerted effort to develop new affordable housing. This could involve public-private partnerships, zoning changes, and innovative financing mechanisms.

In conclusion, given the statistics described above, this is a pivotal year for the Affordable Housing sector. As LIHTC properties near the end of their 30-year compliance period, they face several potential outcomes. Some properties may likely continue as affordable housing due to market conditions, mission-driven ownership, or extended agreements, while others could convert to market-rate housing, particularly in stronger markets. Furthermore, in a declining rate environment the Qualified Contract process could also become more prominent, where existing owners may exist the program, leading to a further reduction in affordable housing stock (especially in high-demand areas). All said and done, we’re clearly at a critical juncture for the affordable housing sector.

RealAssetData has succesffuly connected property tax credits to loan, financial and physical attribute data to provide investors and brokers with the most comprehensive dataset for the Affordable Housing sector.

Disclaimers:

- In analyzing LIHTC roll-offs, it’s important to note that we rely on publicly available federal datasets only.

- All information contained on the website of CREKONNEKT LLC d/b/a RealAssetData (https://realassetdata.com) is protected by U.S. copyright law. Any reproduction or redistribution of this report to a non-subscriber, inside or outside of your firm (if applicable), without the prior written consent of CREKONNEKT LLC is strictly prohibited. The information provided by CREKONNEKT LLC is derived from sources believed to be reliable as of the time of collection; however, it is provided "as is" without any warranty of any kind. CREKONNEKT LLC does not guarantee the accuracy, timeliness, completeness, merchantability, or fitness for any particular purpose of this information. CREKONNEKT LLC is not a broker or investment advisor and does not provide investment advice or recommendations. The information and analysis provided are intended for informational purposes only and should not be considered financial advice. Users are strongly encouraged to conduct independent research and consult with a qualified financial professional before making any investment decisions. By using this information, you agree to these terms and conditions and acknowledge that CREKONNEKT LLC, its affiliates, and its personnel will not be held liable for any errors, inaccuracies, or any damages arising from the use of this information. This includes any direct, indirect, special, consequential, or incidental damages, even if advised of the possibility of such damages. We reserve the right to update this disclaimer at any time.

Powered by Froala Editor

2026-02-24 01:17:42

2026-02-24 01:17:42